G.R. No. 274778, December 3, 2025,

♦ Decision,

Lazaro-Javier, [J]

♦ Separate Opinion Opinion,

Leonen, [J]

♦ Separate Opinion Opinion,

Dimaampao, [J]

♦ Separate Opinion Opinion,

Marquez, [J]

♦ Separate Opinion Opinion,

Villanueva, [J]

♦ Concurring Opinion,

Caguioa, [J]

♦ Concurring Opinion,

Rosario, [J]

♦ Separate and Dissenting Opinion,

Hernando, [J]

♦ Separate Concurring Opinion,

Singh, [J]

♦ Separate Concurring Opinion,

Lopez, [J]

♦ Separate Concurring Opinion,

Gaerlan, [J]

♦ Separate Concurring Opinion,

Inting, [J]

♦ Separate Concurring Opinion,

Zalameda, [J]

EN BANC

[ G.R. Nos. 274778, 275405 & 276233, December 03, 2025 ]

AQUILINO PIMENTEL III; ERNESTO OFRACIO; JANICE LIRZA MELGAR; MARIA CIELO MAGNO; MA. DOMINGA CECILIA B. PADILLA; DANTE B. GATMAYTAN; IBARRA M. GUTIERREZ; SENTRO NG MGA NAGKAKAISA AT PROGRESIBONG MANGGAGAWA; PUBLIC SERVICES LABOR INDEPENDENT CONFEDERATION FOUNDATION, INC.; AND PHILIPPINE MEDICAL ASSOCIATION, PETITIONERS,

ATTY. JOSE SONNY MATULA, PRESIDENT OF THE FEDERATION OF FREE WORKERS (FFW-NAGKAISA LABOR COALITION); DANIEL EDRALIN, SECRETARY GENERAL, NATIONAL VNION OF WORKERS IN HOTEL RESTAURANT AND ALLIED INDUSTRIES (NUWHRAIN-NAGKAISA); RENATO MAGTUBO, CHAIRPERSON, PARTIDO MANGGAGAWA (PM-NAGKAISA); JULIUS CAINGLET, CHURCH-LABOR CONFERENCE, GRACE A. ESTRADA, PRESIDENT, PINAY CAREWORKERS TRANSNATIONAL (PIN@Y); ALFREDO MARANAN, FFW NATIONAL TREASURER; JUN RAMIREZ MENDOZA, UNION PRESIDENT, VISHAY EMPLOYEES PHILIPPINES UNION-FFW AND NATIONAL VICE PRESIDENT, FFW; JUDY ANN CHAN MIRANDA, CHAIRPERSON, NAGKAISA WOMEN COMMITTEE, GENERAL SECRETARY, PM-NAGKAISA; VILMA G. REYES, UNION PRESIDENT, DELA SALLE MEDICAL AND HEALTH SCIENCES INSTITUTE EMPLOYEES UNION-FFW, NATIONAL BOARD MEMBER, FFW; RENE L. CAPITO, NATIONAL PRESIDENT, ALLIANCE OF FILIPINO WORKERS (AFW); ELIJA R. SAN FERNANDO, NATIONAL VICE PRESIDENT, NATIONAL FEDERATION OF LABOR (NFL); RENE DE MESA TADLE, PRESIDENT OF THE COUNCIL OF TEACHERS AND STAFF OF COLLEGES AND UNIVERSITIES OF THE PHILIPPINES (COTESCUP); EMERITO C. GONZALES, UNION PRESIDENT UST FACULTY UNION (USTFU); DENNIES GUTIERREZ, UNION PRESIDENT, INTERPHIL LABORATORIES EMPLOYEES UNION-FFW (ILEU-FFW); ROLANDO LIBROJO, CONVENOR, KILUSANG ARTIKULO 13 (A.13); AND ATTY. DANILO C. ISIDERIO, FFW LEGAL CENTER, PETITIONERS-IN-INTERVENTION,

vs.

HOUSE OF REPRESENTATIVES REPRESENTED BY THE SPEAKER FERDINAND MARTIN ROMUALDEZ; SENATE OF THE REPUBLIC OF THE PHILIPPINES, REPRESENTED BY SENATE PRESIDENT FRANCIS ESCUDERO; DEPARTMENT OF FINANCE SECRETARY RALPH RECTO; EXECUTIVE SECRETARY LUCAS BERSAMIN; AND PHILIPPINE HEALTH INSURANCE CORPORATION REPRESENTED BY ITS PRESIDENT, EMMANUEL R. LEDESMA, JR., RESPONDENTS.

[G.R. No. 275405]

BAYAN MUNA CHAIRMAN NERI COLMENARES, BAYAN MUNA VICE CHAIRMAN TEODORO A. CASIÑO, BAYAN MUNA EXECUTIVE VICE PRESIDENT CARLOS ISAGANI T. ZARATE, AND FORMER BAYAN MUNA REPRESENTATIVE FERDINAND R. GAITE, PETITIONERS,

vs.

*EXECUTIVE SECRETARY LUCAS P. BERSAMIN, SENATE OF THE PHILIPPINES AND THE HOUSE OF REPRESENTATIVES, RESPONDENTS.

[G.R. No. 276233]

1SAMBAYAN COALITION; MEMBERS OF U.P. LAW CLASS 1975 NAMELY: JOSE P.O. ALILING IV, AUGUSTO H. BACULIO, EDGARDO R. BALBIN, MOISES B. BOQUIA, ANTONIO T. CARPIO, MANUEL C. CASES, JR., RICHARD J. GORDON, OSCAR L. KARAAN, BENJAMIN L. KALAW, LUCAS C. LICREIO, TOMAS N. PRADO, ELIZER A. ODULIO, OSCAR M. ORBOS, AURORA A. SANTIAGO, EMILY SIBULO-HAYUDINI, CONRAD D. SORIANO, AND JOSE B. TOMIMBANG; FORMER OMBUDSMAN CONCHITA CARPIO MORALES; SENIOR FOR SENIORS ASSOCIATION, INC., REPRESENTED BY MS. CAROL BLANCO BENAVIDES; KIDNEY FOUNDATION OF THE PHILIPPINES, REPRESENTED BY ATTY. VICENTE GREGORIO; AND ATTY. CHRISTOPHER JOHN P. LAO, PETITIONERS,

vs.

HOUSE OF REPRESENTATIVES REPRESENTED BY THE SPEAKER, FERDINAND MARTIN ROMUALDEZ; THE SENATE OF THE REPUBLIC OF THE PHILIPPINES REPRESENTED BY THE SENATE PRESIDENT FRANCIS JOSEPH ESCUDERO; DEPARTMENT OF FINANCE SECRETARY RALPH RECTO; EXECUTIVE SECRETARY LUCAS BERSAMIN; AND PHILIPPINE HEALTH INSURANCE CORPORATION, REPRESENTED BY ITS PRESIDENT, EMANNUEL R. LEDESMA, JR., RESPONDENTS.

SEPARATE OPINION

DIMAAMPAO, J.:

I concur in the ponencia insofar as it invalidated the transfer of the PHP 60 billion Philippine Health Insurance Corporation (PhilHealth) funds to the National Treasury and directed the return of the said amount to PhilHealth. Nonetheless, I express my reservations regarding the ponencia's decision to defer the resolution of the issue of whether the increase of unprogrammed appropriations from PHP 281.9 billion to PHP 731.4 billion is not unconstitutional. Moreover, I disagree with the wholesale invalidation of Chapter XLIII of the 2024 General Appropriations Act (Special Provision 1(d)) and Department of Finance (DOF) Circular No. 003-2024 and the conclusion that there was an invalid exercise of power of augmentation in this case.

The legal issues relating to the creation, powers, and actions of the BCC must be resolved herein.

At the onset, I must express disagreement regarding the ponente's decision to avoid resolving the issue on "the creation, powers, and actions of the [Bicameral Conference Committee (BCC)]" relative to the enactment of the 2024 General Appropriation Act (GAA) "in order not to preempt" the Court's discussion in G.R. No. 277975, entitled Rodriguez, et al. v. House of Representatives, Senate of the Philippines, and Executive Secretary Lucas P. Bersamin and G.R. Nos. 271059 & 271347 entitled Lagman v. Congress, et al.1 Considering that this legal issue was squarely raised in this controversy—a point which the ponencia itself recognizes2—I submit that the more prudent course of action would be to resolve it once and for all.

For one, there appears to be a notable difference in the legal issues between the two cases. A cursory examination of the relevant arguments in these petitions reveals the nuances in the actions of the BCC that each petition is trying to question. For example, while G.R. No. 277975 concerns the submission of a report with blank items, G.R. No. 275405 brings to the fore the increase in the amount and insertion of a new item in the unprogrammed appropriations, viz.:

| Arguments in G.R. No. 277975 (Rodriguez Petition) pertaining to purported unconstitutional actions of BCC vis-à-vis the 2025 GAA |

Arguments in G.R. No. 275405 (Colmenares Petition) pertaining to purported unconstitutional actions of the BCC vis-à-vis the 2024 GAA |

| IV. REPUBLIC ACT NO. 12116 IS UNCONSTITUTIONAL FOR VIOLATING ARTICLE VI, SECTION 27 OF THE 1987 CONSTITUTION WHEN THE BICAMERAL CONFERENCE COMMITTEE SUBMITTED A REPORT WITH BLANK ITEMS ON THE GENERAL APPROPRIATIONS BILL. |

III. THE BICAMERAL CONFERENCE COMMITTEE COMMITTED GRAVE ABUSE OF DISCRETION AMOUNTING TO LACK OF OR EXCESS OF JURISDICTION WHEN IT:

a. INCREASED THE AMOUNT OF THE UNPROGRAMMED APPROPRIATIONS BY PHP 449.5 BILLION; AND

b. INSERTED A NEW ITEM TO THE SPECIAL PROVISIONS OF THE UNPROGRAMMED FUND.

|

Consequently, in choosing to defer the resolution of issues related to the BCC in the deliberations of G.R. No. 277975 and G.R. Nos. 271059 & 271347, there is a likelihood that specific queries raised herein may not be squarely addressed. Besides, it may not be amiss to point out that the factual circumstances narrated in the present consolidated Petitions serve as the context, and even a crucial parameter, in answering these constitutional questions.

It likewise bears stressing that the two aforecited cases do not appear to have been consolidated by the Court, so the crucial question remains which between these two cases would definitively and actually resolve the core issue.

For another, this course of action, i.e., taking this opportunity to resolve all BCC-related issues herein, completely obviates the need to retroactively apply a potential declaration of unconstitutionality arising from a grave abuse of discretion on the part of the BCC—one of the possible legal outcomes in G.R. No. 277975 or G.R. Nos. 271059 & 271347. In turn, this retroactive application may result in an untenable situation in which the pronouncements in this landmark decision will immediately have to be directly modified by a subsequent ruling.

Incidentally, deferring the resolution of a legal issue to avoid preempting a case that is filed at a later time, and which will be subsequently decided, seems to run counter to fundamental concepts such as the principle of res judicata and litis pendentia, which applies the "barring" effect to the proceedings that were initiated after the first action. In other words, it is the eventual decision in G.R. No. 277975 or G.R. Nos. 271059 & 271347 that should be restricted by the Court's verdict herein, not the other way around.

Accordingly, the ponencia must have considered disposing herein the issues relative to the creation, powers, and actions of the BCC vis-à-vis the 2024 GAA.

As presently drafted, the ponencia is deafeningly silent on the important and timely issue regarding the inclusion of unprogrammed appropriations or budgetary allocations for items or amounts not provided in the NEP.

On this score—and if only for the complete resolution of the issue at hand—I respectfully submit that such increase violates Article VI, Section 25(1) of the Constitution for three reasons:

One. Article VI, Section 25(1) of the Constitution plainly forbids Congress from increasing the appropriations recommended by the President for the operation of the Government as specified in the budget. In as much as the ponencia itself provides that the amount of PHP 281.9 billion unprogrammed appropriations was included in the recommendations of President Ferdinand R. Marcos, Jr. in his budget submissions to Congress,3 then this amount cannot be characterized as anything but an "appropriation[ ] recommended by the President for the operation of the Government" to which the above prohibition applies. Any contrary interpretation, i.e., that only appropriations included in the document known as the BESF may not be increased, would introduce a distinction that is not found in the aforementioned constitutional provision.

In addition, there is neither rhyme nor reason to differentiate between programmed and unprogrammed appropriations, at least as viewed from the lens of the requirement that these projects must originate from and be limited by the amounts set by the Executive branch.

As understood in the budget process, the only divergence between these two is the certainty of funding. Whereas programmed appropriations have a definite or identified funding as of the time the budget is prepared, unprogrammed appropriations refer to those "which provide standby authority to incur additional agency obligations for priority programs or projects when revenue collection exceed targets, and when additional grants or foreign funds are generated."4

However, this is where their dissimilarity ends. There is no significant discrepancy, for instance, in the nature or type of projects that are respectively enumerated in each of these appropriations. Indeed, projects that fall under the former, such as the "strengthening of assistance for government infrastructures and social program" or the "maintenance, repair and rehabilitation of infrastructure facilities,"5 are no different from the projects that fall within the ambit of the latter that also pertain, for instance, to infrastructure facilities.

The lack of distinction on this aspect demonstrates why, similar to that of programmed appropriations, the preparation of unprogrammed appropriations should be subjected to the various steps in the budget preparation phase of the budget cycle.6 In turn, this provides a compelling reason why the changes that Congress must introduce to unprogrammed appropriations cannot also exceed the amounts set by the Executive. Precisely, this gives due regard to the level of evaluation and assessment that they have undergone during budget preparation.

Two. Corollary to the first point, there is no reason why there should be a striking difference in the treatment of the NEP and the BESE To my mind, the NEP is unlike the BESF only because it is not concerned with the specific sources of financing for the proposed projects. This notwithstanding, what is crystal clear is that the NEP is inextricably intertwined with the "BESF" as it contains the details of the government's estimated expenditures, which is the crux of the "BE" portion of the "BESF." In fact, the NEP is so crucial that it even "serves as the basis in the eventual drafting of the general appropriations bill."7

From this perspective, the prohibition against increasing the appropriations recommended by the President applies equally, if not with greater force, to those specified in the NEP. Logically speaking, if it is the NEP that incontrovertibly serves as the "basis" for the general appropriations bill itself, then the appropriations indicated therein are the ones that "must not be increased."

The foregoing leads to no other conclusion other than that the requirement under Article VII, Section 22 of the Constitution of submitting a "budget of expenditure" which would be the "basis of the general appropriations bill," encompasses the contents of the NEP. After all, what is surely more important in the budget process is not the title of a document, but rather the details provided therein. For reference, Article VII, Section 22 reads:

The President shall submit to the Congress within thirty days from the opening of every regular session, as the basis of the general appropriations bill, a budget of expenditures and sources of financing, including receipts from existing and proposed revenue measures. (Underscoring supplied)

Notably, this ties up with my earlier point that the prohibition against increase under Article VI, Section 25(1) should be interpreted to cover all types of appropriations, even unprogrammed appropriations that are only found in the NEP.

Three. Adopting the stance that unprogrammed appropriations are within the purview of Article VI, Section 25(1) and Article VII, Section 22 would irrefutably strengthen safeguards against illicit practices during the budget cycle. By characterizing the recommendation of the President for unprogrammed appropriations as the maximum limit for the said amount, additions or insertions that ultimately give rise to controversies, such as the massive corruption relating to flood control and infrastructure projects that the country is now uncovering,8 would be severely restricted. In theory, these items that would have otherwise been added or inserted would be subjected to more checks. This is because they would also have to undergo the entire budget preparation process in the Executive Department, and not merely the budget legislation phase that is entirely within the hands of Congress.

Upon this point, in determining the amount of the unprogrammed appropriations, the discretion of Congress is always subject to the limits provided under the Constitution. In this case, it comes in the form of the straightforward proscription under Article VI, Section 25(1) that, "Congress may not increase the appropriations recommended by the President for the operation of the Government as specified in the budget."

All told, I submit that the issue of the increase in the amount of unprogrammed appropriations from PHP 281.9 billion to PHP 731.4 billion calls for a direct intervention and must consequently be declared unconstitutional.

The transfer of the PHP 60 billion PhilHealth funds to the National Treasury violates Article VI, Section 29(3) of the Constitution. As part of PhilHealth's reserve funds, these are considered special funds which cannot he lawfully diverted through the invocation of Special Provision 1(d)

I wholeheartedly concur in the ponencia insofar as it declared unconstitutional the transfer of the PHP 60 billion fund balance of PhilHealth to the National Treasury.

Article VI, Section 29(3) of the Constitution states that "[a]ll money collected on any tax levied for a special purpose shall be treated as a special fund and paid out for such purpose only." In CCFOP v. Aquino,9 the Court reiterated that the "revenue collected for a special purpose shall be treated as a special fund to be used exclusively for the stated purpose,11 and cannot be used for any other reason other than such stated purpose.10 Irrefragably, the "Program Reserve Funds" under Section 11 of the Universal Health Care Act (UHCA) may be considered as special funds to which Article VI, Section 29(3) applies.

I expound.

Section 11 of the Universal Health Care Act (UHCA) states:

Section 11. Program Reserve Funds. — PhilHealth shall set aside a portion of its accumulated revenues not needed to meet the cost of the current year's expenditures as reserve funds: Provided, That the total amount of reserves shall not exceed a ceiling equivalent to the amount actuarially estimated for two (2) years' projected Program expenditures: Provided, further. That whenever actual reserves exceed the required ceiling at the end of the fiscal year, the excess of the PhilHealth reserve fund shall he used to increase the Program's benefits and to decrease the amount of members' contributions.

Any unused portion of the reserve fund that is not needed to meet the current expenditure obligations or support the abovementioned programs shall be placed in investments to earn an average annual income at prevailing rates of interest and shall be referred to as the Investment Reserve Fund. The Investment Reserve Fund shall be invested in any or all of the following:

[. . . .]

No portion of the reserve fund or income thereof shall accrue to the general fund of the National Government or to any of its agencies or instrumentalities, including government-owned or -controlled corporations[.]

The above provision outlines the rules concerning the determination and use of the Reserve Funds. It sets a ceiling for these funds, mandating that any surplus be used to boost benefits and lower member contributions. Section 11 also dictates how the Investment Reserve Fund, which is an unused portion of the reserve funds, must be invested. It specifies investment types, such as government bonds and corporate securities, and sets limits on how much can be invested in each.

As astutely pointed out by the ponente, the provision explicitly forbids the transfer of these funds to the National Government's general fund. To quote the ponencia:

The language of Section 11 does not leave PhilHealth any discretion on what to do with their 'reserve funds,' but strictly requires PhilHealth, for the sake of fulfilling their mandate as a public health insurer, to comply with the directives of this provision. Any action contrary to, or outside, the clear dictum of Section 11 of the UHCA is ultra vires, hence, void.

Finally, Section 11 of the UHCA, in no equivocal terms, further commands that "no portion of the reserve fund or income thereof shall accrue to the general fund of the National Government or to any of its agencies or instrumentalities, including [GOCCs]."11

Based on Section 11 of the UHCA, as long as funds are part of PhilHealth's legally defined "reserve funds," they cannot be transferred to the National Government or any of its agencies. This includes contributions from both direct and indirect members, government subsidies, and the earnings from investing these funds.

Here, the constitutional infirmity lies in the transfer of PhilHealth's reserve funds which were transferred using Special Provision 1(d) as basis. For reference, the provision reads:

Special Provision(s)

1. Availment of the Unprogrammed Appropriations. The amounts authorized herein for Purpose Nos. 1, 3-5, and 7-51 may be used when any of the following exists:

. . . .

(d) Fund balance of the Government-Owned or -Controlled Corporation (GOCCs) from any remainder resulting from the review and reduction of their reserve funds to a reasonable levels taking into account disbursement from prior years.

The Department of Finance shall issue the guidelines to implement this provision within fifteen (15) days from effectivity of this Act.

While Special Provision 1(d) mandates the transfer of the fund balance of Government-Owned or -Controlled Corporations (GOCCs) from the remainder which would have resulted from the review and reduction of their reserve funds, such transfer, at least in the case of PhilHealth, may be said to be precluded by Article VI, Section 29(3) of the Constitution because of Section 11 of the UHCA.

During the oral arguments, one line of questioning sought to ascertain whether, taking into consideration the language of Section 11 of the UHCA, PhilHealth's fund balance remitted to the National Treasury could have been sourced from an account separate from its legally defined reserve fund.12 Admittedly, if it was verified that the remitted amount was, in fact, not sourced from Phi [Health's reserve fund, but from a separate, un-earmarked account, then the constitutional prohibition against the use of special funds for any other purpose would have arguably been avoided.

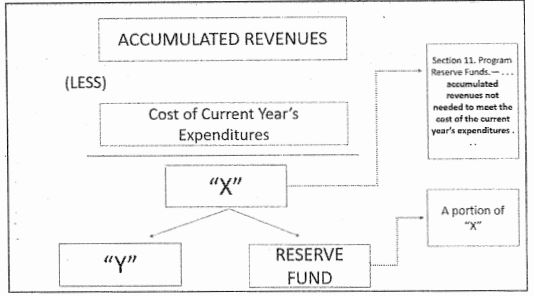

To better illustrate the cited exchange, the diagrams referred to is reproduced herein:

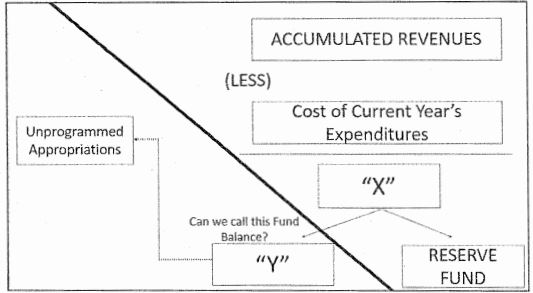

As seen from the above illustrations, there is an essential distinction between PhilHealth's "reserve funds" and "Y," which is the "other portion" of "X." Under Section 11, "X" is the difference between the accumulated revenues and the cost of the current year's expenditures. Verily, the fact that the provision states that the reserve fund is "a portion" of "X" implies that there may be other portions of X that are not necessarily reserve funds, i.e., "Y"

As above adumbrated, the reserve fund is isolated and must remain "untouched" and cannot be transferred to the National Treasury pursuant to Article VI, Section 29(3) of the Constitution. However, the "other portion"—which can be designated as an "excess," "surplus," or the "fund balance"—is not subject to the same limitations. From this analysis, it may therefore be said that it is possible for the government to source funds for unprogrammed appropriations from this "other portion" or "Y," instead of the reserve fund itself.

Such theory may find legal mooring in Department of Finance (DOF) Circular No. 003-2024, which sets forth the guidelines on the implementation of Special Provision 1(d). Specifically, Section 3.1 thereof defines "Fund Balance" as an unrestricted fund, to which "Y" could have qualified. For reference, Section 3.1 reads:

Section 3. DEFINITION OF TERMS

For purposes of these Guidelines, the following definitions shall apply:

1. Fund Balance refers to the unrestricted fund in the form of (i) cash on hand, (ii) cash in banks (e.g., savings account, current account, or time deposits), (iii) investment in government securities, private institutions (e.g., corporate securities and Unit Investment Trust Funds), and other securities, and (iv) other fund balances, including government funds and balances created for specific purposes (e.g., subsidy releases from the National Government and fund transfers from other national government agencies), financial assets (e.g., Treasury Bills, marketable securities, money market funds) and other cash equivalents/investments that are classified under other accounts in the Financial Statements (e.g., Other Assets), subject to the factors as provided in Sections 4.2 and 4.3. (Emphasis supplied)

Atty. Christopher John P. Lao, counsel for petitioner 1Sambayan Coalition et al., however, claims that the foregoing construction was not followed in this case. Verily, the government's actions, specifically in the computation of the funds, suggest that the unprogrammed appropriations may have come from the reserve fund. On the other hand, the Solicitor General agrees that there is a distinction between the reserve funds and the "other portion", stating that the government sources unprogrammed appropriations from these "unrestricted funds", "retained earnings", or the "Y" factor, and not the legally protected reserve funds.

Despite such debate, the matter was definitively settled when Justice Caguioa's incisive interpellation of the Solicitor General himself revealed that the computed PHP 89.9 billion "fund balance" to be remitted to the National Treasury—PHP 60 billion of which were actually already remitted—would originate from PhilHealth's reserve funds. This amount, in turn, is a portion of the PHP 183.1 billion surplus that exceeded the PHP 280.1 billion ceiling set by the DOF when the original, actuarially estimated reserve fund of PHP 463.7 billion was reviewed and reduced in accordance with Special Provision 1(d).13

Likewise, it was determined that in order to comply with Special Provision 1(d), PhilHealth moved this PHP 183.1 billion from its reserve funds account to its surplus or net income account. This was an admission of a deviation from PhilHealth's standard practice, supported by its financial statements, of adding all annual surplus to its reserve funds. Therefore, the PHP 89.9 billion was a portion of funds that, under normal circumstances, would have been considered part of PhilHealth's legally restricted reserve funds.14

Simply put, the oral arguments confirmed that the amount of PHP 60 billion transferred from PhilHealth to the National Treasury originated and formed part of the former's reserve funds. Consequently, such transfer was riddled with infirmity, considering the restrictions placed by the UHCA upon the reserve funds, as well as the disregard of-actuarial computation needed to determine the amount necessary to earmark as reserve funds.

While Special Provision 1(d) cannot be validly invoked to transfer the PHP 60 billion PhilHealth funds to the National Treasury, it may be prudent for the Court to exercise restraint in striking down the same. Declaring if unconstitutional necessitates the invalidation of all other transfers pursuant thereto and the inclusion of a directive regarding their return.

Corollary to its finding that the transfer of the PHP 60 billion PhilHealth fund is invalid, the ponencia also declared Special Provision 1(d) unconstitutional for being an inappropriate provision or rider due to its amendatory effect on the UHCA and the Sin Tax Laws, and for violating Article VI, Section 29(3) of the Constitution.

While there is no denying that the transfer of the PHP 60 billion PhilHealth fund pursuant to Special Provision 1(d) is invalid, I submit that the wholesale invalidation of Special Provision 1(d) should be avoided. As I will elucidate below, the Court should be mindful of the particular context within which the instant constitutional challenge was raised, i.e., vis-à-vis the transfer of the PHP 60 billion from PhilHealth to the National Treasury. As such, its pronouncements herein should not extend beyond the confines of the present controversy.

Prefatorily, it is my view that it would be prudent to avoid categorically declaring Special Provision 1(d) as a rider.

A rider is a provision that is alien or irrelevant to a bill's subject or purpose.15 The rationale against riders in an appropriations bill, as embodied in Article VI, Section 25(2) of the Constitution, is similar to the "one subject, one title" rule under Article VI, Section 26(1). Both constitutional principles require that every provision in a bill be germane or reasonably related to its subject.16

This unity of subject matter is mandatory to prevent hodgepodge or log-rolling legislation, avoid legislative surprise or fraud, and fairly inform the public about the subjects being considered.17 At any rate, the constitutional requirement must be given a reasonable and not an unduly technical meaning.18

Following jurisprudential guidelines, it is clear that Special Provision 1(d) is not a subject alien to the 2024 GAA, in relation to Article VI, Section 26(1) of the Constitution, insofar as it is germane to the law's purpose.

Specifically, the provision functions as a non-appropriation item which does not set aside a specific amount of money. Instead, it places a condition which must first be fulfilled before the amounts authorized—in this case, the fund balances of GOCCs—for the programs identified under Unprogrammed Appropriations may be utilized. Hence, since these funds are directed toward programs already covered by the 2024 GAA, such as those in health, social services, and infrastructure, the provision is germane thereto and is therefore not in the nature of a rider, at least on this ground.

The ponencia, however, premised its ruling that Special Provision 1(d) is a rider on its finding that it amended the UHCA and Sin Tax Laws. Citing Gov. Mandanas v. Hon. Romulo,19 the ponencia maintained that the amendment of existing statutes requires the enactment of a separate law, as Congress cannot effect such changes solely through a provision in the general appropriations measure.20

Respectfully, it is humbly submitted that such conclusion may be avoided through a reconciliation of the foregoing laws.

When confronted with seemingly conflicting statutes, courts should seek to harmonize and reconcile them rather than declaring one invalid. This is because both statutes are products of the same legislature, which is presumed to be aware of existing laws and would expressly state an intent to repeal. Accordingly, all doubts must be resolved against the implied repeal of a statute, and every law should be interpreted in a way that creates a consistent and uniform system of jurisprudence.21 Moreover, repeals by implication are not favored. A repeal is only valid if Congress manifestly intends it or if the laws are so unambiguously inconsistent that they cannot coexist.22

Here, it could be reasonably argued that there is no patent inconsistency between Special Provision 1(d) on one hand, and the UHCA and the Sin Tax Laws on the other for the following reasons:

One. The apparent conflict between the subject laws could have been avoided if the DOF had sourced PhilHealth's "fund balance" from the "other portion", which is essentially distinct from its reserve funds. As exhaustively discussed, the Section 11 of the UHCA. designates the reserve fund as only one "portion" of the total accumulated revenues left over after covering current expenditures. Thus, while such portion must remain, by law, untouched, there is another portion, or the "Y" factor as labeled previously, which is unrestricted.

To my mind, the existence of such interpretation means that the two provisions can stand together.

True, both Special Provision 1(d) and DOF Circular No. 003-2024 make use of the term "reserve fund", which as mentioned, is a distinct fund under the UHCA given the well-defined parameters under Section 11 thereof. Nonetheless, Section 3.1 of DOF Circular No. 003-2024—which, to reiterate provides the guidelines in implementing Special Provision 1(d)—defines "Fund Balance" as an "unrestricted fund." Accordingly, vis-à-vis PhilHealth, this simply means that the Fund Balance must originate from the unrestricted "Y" portion in the diagram above. Appositely, the directive that "[i]n computing the Fund Balance, a reasonable level of Reserve Funds must be maintained by the GOCC," should then be interpreted to mean that, anent PhilHealth, the Program Reserve Fund must remain untouched.

Two. The bedrock principle of statutory construction, "Generalia specialibus nan derogant"23 ("A general law does not derogate from a special one"), applies to the apparent irreconcilability between Special Provision 1(d) and the UHCA and the Sin Tax Laws. Upon this point, a general law and a special law on the same subject are statutes in pari materia, and should be read together and harmonized, if possible, with a view to giving effect to both. The general law will yield to the special law in the specific and particular subject embraced in the latter.24

The 2024 GAA is a general law providing for the government's overall budget, while the UHCA and the Sin Tax Laws are special statutes governing the specific funding and operation of the National Health Insurance Program. Special Provision 1(d) of the 2024 GAA and the UHCA and the Sin Tax Laws must be read and construed together, then, by taking the UHCA and Sin Tax Laws as exceptions to the general law in order to reconcile them. Consequently, the UHCA and the Sin Tax Laws, as special laws, should prevail with respect to the use of excess reserve funds, as a general law does not repeal a special law by implication.

The same reasoning applies to the Sin Tax Laws, in relation to the limitations imposed by Article VI, Section 29(5) of the Constitution. The ponencia invalidated Special Provision 1(d), with respect to the Sin Tax Laws, on the ground that it violated the prohibition against disbursing special funds for anything other than a special purpose. However, the specific purpose for which these revenues were collected cannot be subverted by Special Provision 1(d). The provision is a general statement that refers only to a general class of entities, i.e., GOCCs, and a general process to "review and reduce" reserve funds. This is not the clear and express statement of repeal required by law to override a special statute. As such, the presumption against implied repeal applies with full force.

Three. The very language of the statutes resolves any apparent conflict. A textual analysis reveals a clear hierarchy among the mandatory duties imposed by the UHCA and Sin Tax Laws, on one hand, and the discretionary authority granted by Special Provision 1(d), on the other. The use of the word "may" in the latter signifies that this is a permissive or discretionary power, not a mandatory directive. It grants the Executive, specifically the DOF and the Department of Budget and Management, the discretion to act, but does not compel them to do so. This is in stark contrast to the UHCA and the Sin Tax Laws, which contains mandatory language that PhilHealth shall establish a reserve fund and that specific portions of the Sin Tax collections shall be used for implementation of the UHCA.

The specific, non-discretionary nature of the UHCA's mandate for a reserve fund reinforces the above interpretation: "PhilHealth shall set aside a portion of its accumulated revenues not needed to meet the cost of the current year's expenditures as reserve funds: Provided, That the total amount of reserves shall not exceed a ceiling equivalent to the amount actuarially estimated for two (2) years' projected Program expenditures."25 Verily, the UHCA is based on actuarial principles and studies to ensure the long-term viability of the National Health Insurance Program.

In sum, the discretionary power to "review and reduce" cannot be used to defeat a specific and scientifically based legal requirement. Considering the mandatory application of actuarial principles and studies, the "reasonable levels" for PhilHealth's reserve funds are simply not subject to mere executive review. Such are determined by a specific law to be actuarially sound. For the Executive to "reduce" these funds based on a general provision in the 2024 GAA would be a direct violation of the UHCA's legal and actuarial mandate.

The use of mandatory language in a statute was well-explored in Guiao v. PAGCOR,26 likewise cited in the ponencia. In that case, the Philippine Sports Commission's (PSC) Charter mandated that "five percent (5%) of the gross income ... shall be automatically remitted." However, PAGCOR was remitting a lesser amount based on an executive memorandum. The Court decisively ruled that a clear, mandatory statutory provision could not be subverted by an executive issuance. Hence, when a law establishes a definitive policy with mandatory language, that policy takes supremacy over any discretionary directive in a separate law or executive issuance.

The same conclusion may be drawn in this case. As in the PSC's charter analyzed in Guiao, the Sin Tax Laws are worded without qualification, thereby removing any discretion from the respondents.(awÞhi( They are obligated to account for the percentage of sin tax collections earmarked for the UHCA and ensure that this specific amount is allocated to PhilHealth in the general appropriations law.

In sum, far from impliedly repealing the UHCA and the Sin Tax Laws, a mere discretionary power granted to the Executive branch under Special Provision 1(d) cannot subvert clear and mandatory legislative policies. The discretion to "review and reduce" cannot be interpreted as a power to contravene the specific purpose of the funds as defined by a special laws. Verily, Special Provision 1(d) is best interpreted as being inapplicable to GOCCs like PhilHealth.

Proceeding from the discussion, the total invalidation of the legal provision based on the theory that the same is an inappropriate provision is unwarranted. As discussed, it does not appear to be imperative to declare Special Provision 1(d) as unconstitutional per se. To reiterate, its perceived infirmity arises only when the same is improperly used as basis to divert special funds under the UHCA and the Sin Tax Laws.

In addition to the above suggestion regarding the possible construction of these seemingly conflicting set of laws, the Court must be mindful that it should constantly strive to exercise judicial restraint. Thus, it must refrain from nullifying an act of a co-equal branch where the ostensible violation may be remedied by some other way without declaring the provision invalid. Here, the return of the PHP 60 billion PhilHealth funds may be achieved by holding that it was grave abuse of discretion on the part of the DOF to invoke Special Provision 1(d) in transferring the said money to the National Treasury, even sans the concomitant invalidation of the legal provision.

This tempered approach recognizes that Special Provision 1(d), as worded and as previously mentioned, does not solely apply to PhilHealth, but also to all other GOCCs. For instance, as brought up by the Solicitor General, Special Provision 1(d) was also applied against PDIC's reserve funds,27 resulting in the remittance of the amount of PHP 107.23 billion from its unrestricted funds.28

Accordingly, it must be accentuated that the wholesale invalidation of Special Provision 1(d) carries far more significant implications beyond PhilHealth. For one, it suggests that the remittances already made by other GOCCs, like PDIC as mentioned—which did not necessarily breach any prohibition on the use and transfer of their own reserve funds—must also be reversed, despite there being no unique constitutional or statutory basis to compel a refund in those cases. For another, unlike in PhilHealth's case, the ponencia did not undertake the same thorough analysis of these other GOCCs' separate charters or their statutory definitions of reserve funds. Hence, it is entirely possible that the laws governing these other GOCCs, such as the PDIC, may permit, or otherwise can be interpreted, to allow for such remittances to the National Treasury. This unintended, or even untenable implications, as well as the lack of individualized scrutiny over other GOCCs, only confirms that the declaration of unconstitutionally should have been strictly confined to the specific transfer of PhilHealth's reserve funds.

At the very least, as the ponencia is of the position that Special Provision 1(d) is unconstitutional per se, other transfers to GOCCs pursuant thereto must also be struck down and they must be instructed to return the transferred money.

Special Provision 1(d) is not-unconstitutional on the basis of an invalid exercise of power of augmentation.

The ponencia also hinged its determination that Special Provision 1(d) is unconstitutional on the fact that it violated Article VI, Section 25(5). In this regard, the Secretary of Finance supposedly exercised the power of augmentation exclusively belonging to the President.

I respectfully disagree.

The appropriation under Special Provision 1(d) and the transfer of savings under Article VI, Section 25(5) of the Constitution are fundamentally distinct legal concepts. The fact that Special Provision 1(d) did not meet any of the requisites for a valid augmentation does not automatically mean that what transpired is a breach of the said Constitutional provision. Contrary to the ponencia's postulation therefore, this is not a case in which the "very infirmity" of the act is used "as a defense."29 Instead, it means that it is not the type of transaction that is covered by the constitutional provision in the first place.

The power of augmentation under Article VI, Section 25(5) of the Constitution is a limited and exceptional power granted to specific officials, i.e., the President, heads of the Senate and House, the Chief Justice, and heads of Constitutional Commissions. This power is strictly confined to the transfer of savings from one appropriation item to another within the same office.

In contrast, Special Provision 1(d) is not an agency-specific appropriation that is contemplated in Article VI, Section 25(5) of the 1987 Constitution. Otherwise started, it does not deal at all with the use of savings of an office to "augment" another item in its respective appropriation. As mentioned, it instead serves as one of the four eventualities in which the amounts authorized under unprogrammed appropriations may be used. In met, as earlier defined, unprogrammed appropriations "provide standby authority to incur additional agency obligations for priority programs or projects when revenue collection exceed[s] targets, and when additional grants or foreign funds are generated."30

Moreover, it bears stressing that the ponencia's analysis leads to the invalidation of the entire Special Provision 1. Its discussion in p. 113-115 of the ponencia, for instance, may be likewise used to invalidate Special Provision 1(a) relating to "excess revenue collections in the total tax revenues or any one of the identified non-tax revenue sources from its corresponding revenue collection target, as reflected in the 2024 BESF submitted by the President," for the simple reason that none of the requisites under Section 25(5) have been complied with despite the fact that there is also movement of money in this instance.

In sum, examining Special Provision 1(d) against the standards set by Article VI, Section 25(5) of the Constitution would be akin to judging a fish by its ability to climb a tree. Stated differently, such criteria are simply and outrightly inapplicable, and even irrelevant in this case.

A final cadence. I agree with the inclusion of the directive to return the amount of PHP 60 billion to be returned to PhilHealth. Aside from the representations from the Executive Department that the government will comply31 with the orders of the Court in this case, the operative fact doctrine is, at its core, a rule of equity.32 As such, it is "applied in circumstances where the nullification of the effects of what used to be a valid law would result in inequity and injustice."33 While the Court has applied the said doctrine several times in cases involving constitutional questions relating to the budget,34 the biggest "inequity and injustice" in this case would be to deprive the Filipino people of an actual redress in the face of a violation of their right to health.

Nonetheless, it would appear that the same consideration may not be present with respect to the declaration of unconstitutionality of Congress' increase of the Unprogrammed Appropriation from PHP 281.9 billion to PHP 731.4 billion. Among others, this is an issue that is completely independent from the violation of the right to health. As well, the money herein may have already been used to fund various projects that can no longer be undone. Hence, the operative fact doctrine will not apply.

Footnotes

1 Ponencia, p. 36.

2 Id.

3 Id. at 10. "House Bill No. 8980 adopted the PHP 5.7676 trillion budget, with PHP 4.0198 trillion programmed appropriations, PHP 1.7478 trillion automatic appropriations, and PHP 281.9 billion unprogrammed appropriations, as recommended by President Marcos, Jr. in his budget submissions." (Emphasis supplied) Id.

4 See Department of Budget and Management, OFTEN MISCONSTRUED BUDGET TERMINOLOGIES, available at https://www.dbm.gov.ph/wp-content/uploads/2012/03/PGB-B6.pdf (last accessed September 28, 2025).

5 Republic Act No. 11975 (2024), General Appropriations Act, Chapter XLIII, pp. 739-740. See Unprogrammed Appropriations, available at https://www.dbm.gov.ph/wp-content/uploads/GAA/GAA2024/VolumeI/UA.pdf (Iast accessed September 28, 2025).

6 See Araullo v. Aquino III, G.R. Nos. 209287, et al., July 1, 2014 [Per J. Bersamin, En Banc].

7 Department of Budget and Management, GLOSSARY OF TERMS, https://www.dbm.gov.ph/wp-content/uploads/BESF/BESF2024/GLOSSARY.pdf (last accessed October 27, 2025) GLOSSARY.pdf, p. 866.

8 20th Congress of the Senate of the Philippines, Lacson Pushes Ban on Infra Project Insertions in Budget,

September 21. 2025, available at https://web.senate.gov.ph/press_release/2025/0921_lacson2.asp (last accessed September 28, 2025).

9 G.R. No. 217965, August 8, 2017 [J. Mendoza, En Banc].

10 Id.

11 Ponencia, p. 61-62.

12 ASSOCIATE JUSTICE DIMAAMPAO:

Is it accurate to say that the difference of accumulated and the cost of current year's expenditures is the "reserve fund"? Is that an accurate statement?

. . . .

GOVERNMENT CORPORATE COUNSEL HERMOSURA:

The reserve fund is the accumulated ... is taken from the past years.

ASSOCIATE JUSTICE DIMAAMPAO

So, it's not accurate because, as the law says, [a] "portion". So that reserve fund is just a portion of the difference between accumulated revenues and cost of current year's expenditures.

Now, since the reserve fund is just a portion, let's label that as "X". So how do you now term that "X"? [...] Can you think of a term that will describe the difference between accumulated revenues and cost of current year's expenditures, given that reserve funds is just a portion of that? Can you think of a term, inasmuch as the law does not mention any term about such difference? [...]

GOVERNMENT CORPORATE COUNSEL HERMOSURA:

Actually, the current year's expenditures are matched against the current year's revenue. You Honor.

ASSOCIATE JUSTICE DIMAAMPAO

Can we use this word "excess"? [...] In the absence of a clear term, "excess" of accumulated revenues and cost of current year's expenditures. From that excess, a "portion" forms part of the reserve fund.

GOVERNMENT CORPORATE COUNSEL HERMOSURA:

Actually, the COA also uses the term "surplus".

ASSOCIATE JUSTICE DIMAAMPAO

Okay, last week, I heard the term ""gap". There is a "gap". Now, you are espousing the theory that should be termed as "surplus". The literal term is "excess". Is the word "surplus" appropriate to describe such excess? What do you mean by "surplus"?

. . . .

ASSOCIATE JUSTICE DIMAAMPAO

Okay, in any case, since the law provides no clear term that will describe excess or surplus, as the case may be, so when it says "portion", so there is that "other portion". Do you agree?

SOLICITOR GENERAL GUEVARRA:

Yes, You Honor.

ASSOCIATE JUSTICE DIMAAMPAO

Okay, so we can label that as "Y". Now, can you think of a technical term that will describe that "other portion"? So, literally, it's "other portion" because the [...] portion [pertaining to the] reserve fund is another one. So let's label it as "Y". [...]

Hermosura:

Actually, we can replace that diagram with like, say. Your Honors, a circle, like a pie. So the pie represents the total accumulated revenues. That total accumulated revenues, you can slice it into parts: one part is called the "reserve fund". So in this case, the total pie is 500 billion. And then you take a slice of that total pie, make it into the reserve funds. That's the 280 [billion]. [...] And then the [...] remainder of this pie, that's the fund balance, actually.

ASSOCIATE JUSTICE DIMAAMPAO

Fund balance?

GOVERNMENT CORPORATE COUNSEL HERMOSURA:

Yes.

ASSOCIATE JUSTICE DIMAAMPAO

So, you mean "Y" can also be considered fund balance?

GOVERNMENT CORPORATE COUNSEL HERMOSURA:

Yes, yes. That's correct, Your Honor. [...]

. . . .

ASSOCIATE JUSTICE DIMAAMPAO

Given this PowerPoint Presentation, [...] is it not possible that the source for unprogrammed appropriations may come from "Y", which we label [...] "other portion"? [...]

ATTY. LAO:

You Honor, for me, [...] per admission by the government, [...] as labelled in the GAA, the one that was taken away, the 60 billion, so far, came from Sin Taxes, Your Honor, because the GAA says this is the appropriation for Sin Taxes.

ASSOCIATE JUSTICE DIMAAMPAO

Just answer yes or no.

ATTY. LAO:

No, Your Honor.

ASSOCIATE JUSTICE DIMAAMPAO

The reserve fund is isolated. It must remain untouched. That's why there is a barrier there, which implies that reserve fund must be untouched, isolated form the other portion.

Now, the Solicitor General, please, is that me one that the government has been doing? That it may source such unprogrammed appropriation from the other portion.

SOLICITOR GENERAL CUEVARRA:

Exactly, Your Honor.

ASSOCIATE JUSTICE DIMAAMPAO

Not the reserve fund?

SOLICITOR GENERAL GUEVARRA:

No, because the DOF Circular clearly stated that the GOCCs shall review and reduce to a reasonable level their reserve funds, making into account their historical expenditures from the previous years. And the remainder—meaning, outside the reduced or reasonably reduced reserve fund—will be the base for the computation of what should be remitted back to the Treasury.

And in that particular example. Your Honor, [that is] your "Y" factor, which refers to accumulated revenues over the past years. In the case of the PDIC, which is the other GOCC that remitted funds to the National Treasury. These are the unrestricted funds, these are the retained earnings of PDIC. Precisely, your "Y" factor And that was the amount determined to be returned to the treasury.

ASSOCIATE JUSTICE DIMAAMPAO

Any refutation?

ATTY. LAO:

Yes, Your Honor, in the Bureau of Treasury's presentation for the House of Representatives on May 8, 2024. They determined the fund balance [...] from 2021 to 2023 as premium for indirect contributors minus benefit claims [...].

ASSOCIATE JUSTICE DIMAAMPAO

We have repeatedly mentioned "fund balance", where in that presentation is the fund balance?

ATTY. LAO:

That's actually my quandary. Your Honor, because they based on the presentations, they just computed it on their subsidy minus benefit claims of indirect contributors. That's it. [...]

ASSOCIATE JUSTICE DIMAAMPAO

Will you espouse the theory that it may come from the reserve fund?

ATTY. LAO:

Yes, Your Honor.

13 Ponencia, p. 66.

14 Id. at 66-67.

15 Atitiw v. Zamora, 508 Phil. 321 (2005) [Per J. Tinga, En Banc].

16 Saint Wealth Ltd. v. Bureau of Internal Revenue, G.R. Nos. 252965 & 254102, December 7, 2021 [Per J. Gaerlan, En Banc].

17 Id.

18 Sinsuat v. Ebrahim, G.R. Nos. 271741 & 271972, August 20, 2024 [Per J. Zalameda, En Banc].

19 473 Phil. 806 (2004) [Per J. Callejo, Sr., En Banc].

20 Ponencia, p. 54.

21 Bangko Sentral ng Pilipinas v. Commission on Audit, G.R. No. 210314, October 12, 2021 [Per J. Hernando, En Banc].

22 Id.

23 Tomawis v. Hon. Balindong, G.R. No. 182434, March, 5, 2010 [Per J. Velasco, Jr., En Banc].

24 Id.

25 Section 11, UHCA.

26 Guiao v. Philippine Amusement and Gaming Corp., G.R. No. 223845, May 28, 2024 [Per S.A.J. Leonen, En Banc].

27 ASSOCIATE JUSTICE DIMAAMPAO

The reserve fund is isolated. It must remain untouched. That's why there is a barrier there, which implies that reserve fund must be untouched, isolated form the other portion.

Now, the Solicitor General, please, is that the one that the government has been doing? That it may source such, unprogrammed appropriation from the other portion.

SOLICITOR GENERAL GUEVARRA:

Exactly, Your Honor.

ASSOCIATE JUSTICE DIMAAMPAO

Not the reserve fund?

SOLICITOR GENERAL GUEVARRA:

No, because the DOF Circular clearly stated that the GOCCs shall review and reduce to a reasonable level their reserve funds, taking into account their historical expenditures from the previous years. And the remainder—meaning, outside the reduced or reasonably reduced reserve fund—will be the base for the computation of what should be remitted back to the Treasury.

And in that particular example, Your Honor, [that is] your "Y" factor, which refers to accumulated revenues over the past years. In the case of the PDIC, which is the other GOCC that remitted funds to the National Treasury. These are the unrestricted funds, these are the retained earnings of PDIC. Precisely, your "F" factor. And that was the amount determined to be returned to the treasury.

28 See Department of Finance, PDIC remittance to the national government supports national development while maintaining a sound deposit insurance system, January 12, 2025, available at https://www.dof.gov.ph/pdic-remittance-to-the-national-government-supports-national-development-while-maintaining-a-sound-deposit-insurance-system/ (last accessed September 27, 2025).

29 Ponencia, p. 115.

30 See Department of Budget and Management. OFTEN MISCONSTRUED BUDGET TERMINOLOGIES. available at https://www.dbm.gov.ph/wp-content/uploads/2012/03/PGB-B6.pdf (last accessed September 28, 2025).

31 Ponencia, p. 124.

32 Id. at 122.

33 Id.

34 See e.g. Belgica v. Ochoa, G.R. Nos. 208566, 208493 & 209251, November 19, 2013 [Per J. Perlas-Bernabe, En Banc].

The Lawphil Project - Arellano Law Foundation